Carmignac Sécurité: Letter from the Fund Manager

![[Management Team] [Author] Allier Marie Anne](https://carmignac.imgix.net/uploads/NextImage/0001/18/%5BManagement-Team%5D-Allier-Marie-Anne.png?auto=format%2Ccompress&fit=fill&w=3840)

Carmignac Sécurité lost –3.18% in the second quarter of 2022, while its reference indicator¹ was down –1.30%.

Quarterly Performance Review

The first quarter of this year may have been one of the worst for bond markets in the past five decades, but the second quarter was even more calamitous. The reasons for the steep losses were the same in both quarters (or at least until mid-June):

1) The war between Russia and Ukraine isn’t letting up, which is adding uncertainty, inflationary pressure (e.g. through higher food and energy prices), and economic growth worries as a result of embargos (on oil) and disruptions to the supply of natural gas, minerals, fertiliser, and more.

2) Inflation isn’t coming down; the timing of peak inflation keeps getting pushed back month after month.

3) Central banks are stepping up the pace of policy tightening in response, in order to prevent inflation expectations from becoming unanchored.

- The Fed has begun its cycle of rate hikes and even accelerated the process in June. It’s also shrinking its balance sheet by selling bonds in an attempt to amplify the contractionary effects of its measures.

- The ECB is struggling to keep pace but announced it would end its asset purchases in July (after scaling them back gradually in Q2). It’s expected to carry out its first rake hike at its end-July meeting.

- Most other central banks have embarked on the same trajectory. This trend of monetary policy tightening around the world marks a real shift away from the policy of the past 15 years.

Looking specifically at the eurozone, inflation came in at over 8% in May year-over-year, but with stark country-by-country differences (22% in Estonia, 6.5% in France, 10% in Spain, and 8.5% in Germany, for example). Inflation isn’t expected to peak until this autumn, unless the timing gets pushed back again, as it has been several times in the past year or more.

The ECB has therefore begun pulling the strings on monetary policy – but while also attempting to mitigate the effects of the tightening on sovereign credit spreads. It’s logical that the most indebted countries would be hit hardest by the end of bond purchases, but in mid-June the ECB – in light of the magnitude (and probably also the speed) of the jump in spreads – had to promise it would introduce a mechanism to put a cap on the widening. For now, no concrete measures have been revealed except for greater flexibility in how it will reinvest the assets on its balance sheet. The ECB Governing Council is probably still hammering out the details. But in any case, just the announcement that an instrument was in the works was enough to spark a mini rally in the spread between Italian BTPs and German Bunds starting in mid-June.

At that point, the trends that had been prevailing in financial markets since late March went into reverse. Sovereign bond yields had been rising sharply, with the 10-year Bund yield climbing 125 bp to 1.80% at mid-June and the 2-year Bund yield up 131 bp to 1.23%; the BTP-Bund spread on 10-year paper had reached 241 bp. But concerns that central banks would go too far in their policy tightening and end up triggering a recession changed all that. The 10-year Bund yield fell 45 bp and ended Q2 at 1.35%, while that on 10-year BTPs fell from 4.18% to 3.26% (or a nearly 50 bp drop in the spread).²

Corporate bond yields, however, didn’t make the same U-turn. The spread on high-yield paper widened 240 bp during the quarter and that on investment grade issues rose 45 bp, on the back of fears about a recession and the possibility that Russia could cut off natural gas supplies.² Individual sectors also faced specific headwinds; businesses highly sensitive to interest rates (like those in the real estate sector) were hit by the increase in borrowing costs.

Fund Performance

Our Fund’s performance in Q2 can be divided into two distinct phases. In phase one, our portfolio held up well against the market downturn even though the absolute return was negative (–0.95% at 10 June, against –1.92% for its reference indicator). We were able to outperform the market during this phase thanks to our low modified duration, our credit protection (through CDS Xover indices), our negative exposure to Italy (and to peripheral spreads in general), and our investments on inflation. Few major changes were made to our portfolio in this phase – we kept its modified duration in the conservative range of 0.30–0.70, we shored up our short positions on Italy, we had protection on around 10% of our credit holdings, and cash and cash equivalents amounted to around 35% of the Fund’s assets.

That was phase one. In phase two, which began in mid-June, the about-face in fixed income markets caught our portfolio off guard. The low modified duration meant we couldn’t benefit from the decrease in yields; our short positions on core countries (the US, Germany, and to a lesser extent France) dented our returns; and most of all, the level (and type) of credit protection we had didn’t adequately shield our credit book. In those last two weeks of June, our Fund lost all of the lead it had on the market and even deepened its losses to end the quarter well into negative territory. The decline in yields suggests investors no longer believe central banks will be able carry out their rate hikes (even though central bankers consistently stress that combating inflation is their top – if not their only – priority). Two weeks of worries about economic growth have wiped out six months of inflationary fears. Compounding the problem is the reduced amount of liquidity in the market (because of the H1 close and the withdrawal of central banks), which has created dislocations in some credit market segments – for example, cash and credit derivatives are no longer correlated, and prices have fallen dramatically for some issuers and in some sectors. Even though we increased our level of credit protection to 15% during this phase, and despite our high percentage of cash holdings, our Fund didn’t come out of the period unscathed.

In Q2 (unlike in Q1), our remaining Russian holdings didn’t have much of an effect on our returns. We offloaded investments in the Russian complex during the quarter so that they amounted to just 0.8% of the portfolio at end-June; we sold Russian sovereign paper at around 17 cents on the dollar and Gazprom bonds at around 30 cents.

What is our outlook for the coming months?

We currently believe that central banks won’t let their guard down just yet (the Fed and ECB “pivot” that market participants are expecting to happen soon) and have positioned our portfolio accordingly, with low sensitivity to interest rates and specially to core countries. And because this stance by central bankers could have a potentially significant impact on growth (a fact of which they seem fully aware), we have maintained a high level of credit protection and a substantial cash allocation.

Our performance drivers in the coming months will be:

- Low modified duration with a short bias on eurozone sovereigns (Germany, France, Italy, and Spain) since the ECB will probably remain focused on taming inflation, at least in the near term;

- A corporate bond allocation centered on three convictions: energy, financials, and CLOs;

- High credit protection, since the combination of weaker GDP growth, high inflation, high interest rate volatility, and worries about a cut-off of natural gas supplies will handicap credit markets in the near term, despite the increasingly attractive valuations;

- An over 30% allocation to cash and cash equivalents, enabling us to once again seize investment opportunities as soon as we have more visibility.

- Residual exposure to Russia (mainly Gazprom), which we will reduce further when prices are no longer being impacted by a dislocated market and extremely harsh implied recovery rates.

- An average yield on our portfolio that now sits at 3.56% – the highest in nearly ten years – reflecting our Fund’s capacity to generate returns in the coming months.

¹Reference indicator: ICE BofA 1-3 Year All Euro Government Index (coupons reinvested). ²Source: Carmignac, Bloomberg au 31/03/2022.

Carmignac Sécurité

Flexible, low duration solution to challenging European marketsDiscover the fund pageRendement

| Carmignac Sécurité | 2.1 | 0.0 | -3.0 | 3.6 | 2.0 | 0.2 | -4.8 | 4.1 | 5.3 | 0.7 |

| Referentie-indicator | 0.3 | -0.4 | -0.3 | 0.1 | -0.2 | -0.7 | -4.8 | 3.4 | 3.2 | 0.7 |

| Carmignac Sécurité | + 3.2 % | + 2.4 % | + 0.9 % |

| Referentie-indicator | + 1.1 % | + 0.4 % | + 0.1 % |

Bron: Carmignac op 31 mrt. 2025.

In het verleden behaalde resultaten zijn geen garantie voor de toekomst. De resultaten zijn netto na aftrek van kosten (inclusief mogelijke in rekening gebrachte instapkosten door de distributeur) .

Referentie-indicator: ICE BofA 1-3 Year All Euro Government index

Carmignac Sécurité AW EUR Acc

- Aanbevolen minimale beleggingstermijn

- 2 jaar

- SFDR-fondscategorieën**

- Artikel 8

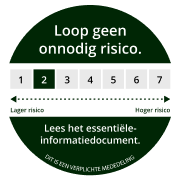

- Risicoschaal*

*Risicocategorie van het KID (essentiële-informatiedocument) indicator. Risicocategorie 1 betekent niet dat een belegging risicoloos is. Deze indicator kan in de loop van de tijd veranderen. **De Sustainable Finance Disclosure Regulation (SFDR) 2019/2088 is een Europese verordening die vermogensbeheerders verplicht hun fondsen te classificeren zoals onder meer: artikel 8 die milieu- en sociale kenmerken bevorderen, artikel 9 die investeringen duurzaam maken met meetbare doelstellingen, of artikel 6 die niet noodzakelijk een duurzaamheidsdoelstelling hebben. Voor meer informatie, bezoek: https://eur-lex.europa.eu/eli/reg/2019/2088/oj?locale=nl.

Voornaamste risico's van het Fonds

Recente analyses

Carmignac Portfolio Sécurité: Brief van de Fondsbeheerders

Carmignac Sécurité: Brief van de Fondsbeheerders